Choosing the right business structure for your new venture is a crucial decision. Many business owners lean toward two of the most popular options—LLCs and sole proprietorships.

Each one has its fair share of benefits and drawbacks.

The right one for you and your business will depend on several factors. You’ll need to consider things like the tax implications, startup costs, regulations, liability protection, and more.

If you’re torn between the two, you’ve come to the right place. This guide will provide you with an in-depth explanation of LLCs and sole proprietorships. You’ll learn more about each one’s advantages, potential downsides, and the differences between the two.

What is an LLC?

LLC stands for “limited liability company.”

These are legal entities formed at the state level. When you start an LLC, you’ll have to decide where you want to register it. For most of you, that answer is simple—your home state will almost always be the best option.

LLCs are popular because they combine some of the positive aspects of corporations and partnerships while eliminating some drawbacks of each. Like a corporation, LLC owners and shareholders benefit from limited liability protection (hence the name). LLCs also provide pass-through taxation, like a partnership.

Types of LLCs

There are several different categories within LLCs. Generally speaking, you’ll need to choose one option from each of the following four categories:

- Single-Member LLC vs. Multi-Member LLC — As the name implies, a single-member LLC (SLLC) has one owner. The IRS treats SLLCs like a sole proprietorship, in the sense that the owner doesn’t have to file separate taxes (note that this is not always the case at the state level). Partnerships would fall into the multi-member LLC category. Multi-member LLCs must file separate tax returns and have contingencies in place for events like death, split-ups, and irreconcilable disagreements.

- Member-Managed LLC vs. Manager-Managed LLC — Most LLCs are member-managed, meaning that the owner (or owners) run the business. Managers (not owners) named in the LLC operating agreement run a manager-managed LLC. This structure allows owners to distance themselves from the company’s operational tasks. Investors who are family members or silent partners may want to form a member-managed LLC.

- Regular LLC vs. Professional LLC — Some states don’t allow certain professions to form an LLC. Doctors, lawyers, CPAs, chiropractors, and similar businesses may be required to form a PLLC (professional LLC). Only licensed professionals can be listed as members of a PPLC.

- Domestic LLC vs. Foreign LLC — Domestic LLC refers to the state where the LLC is formed. For example, if an LLC is registered in Colorado and does business in Colorado, it’s a domestic LLC. But if that same business is registered in Nevada (to do business in Colorado), it’s operating as a foreign LLC. Many owners look to form LLCs in “tax-friendly” states. But this usually requires the formation of two LLCs—one in the state of registration and another in the business owner’s home state (a foreign LLC).

All LLCs will have one of the designations from each bullet listed above. For example, you could have a domestic, single-member PLLC that is member-managed.

What is a Sole Proprietorship?

Sole proprietorships are a bit more straightforward than an LLC.

A sole proprietorship is owned and run by a single person. This business structure is unincorporated, meaning that the company is not considered a separate legal entity. At both the federal and state levels, business owners and sole proprietors are viewed (and taxed) as one and the same.

According to a recent study, there are more than 23 million sole proprietorships in the United States. This number represents 73% of all business structures in the country—making it the most popular organizational structure.

Many sole proprietors are also independent contractors (freelancers), although the two terms are not synonymous. Independent contractors work for another business, but not as an employee.

By default, the legal name of a sole proprietor’s business is their own name. Many owners choose to register a DBA (doing business as) name to add professionalism to a sole proprietorship.

For example, let’s say you’re a sole proprietor named Joseph Johnson that provides marketing consulting services. You could register a DBA called “JJ Marketing Associates” to avoid using your name for business purposes, marketing purposes, or as the public-facing name of the company.

Even with a DBA, the state and federal government doesn’t recognize your sole proprietorship as a separate entity.

Similarities Between LLCs and Sole Proprietorships

When comparing LLCs and sole proprietorships side-by-side, it’s important to recognize that these two business structures share some commonalities.

Here’s a quick list of the similarities between LLCs and sole proprietorships:

- Income and expenses must be reported in Schedule C Form 1040.

- Net income is taxable, regardless of whether or not cash is withdrawn from the business.

- They have similar rules for tax deductions (like home office expenses and health insurance premiums).

- An EIN (employer identification number, also known as a tax ID number) must be obtained if employees are hired.

- Any industry-specific business licenses and permits at the state and federal levels are still required.

- LLCs and sole proprietors both have the option to register a DBA (doing business as) name.

As you can see, from taxation to paperwork filing, LLCs and sole proprietorships do have a handful of things in common.

Differences Between LLCs and Sole Proprietorships

Now it’s time to compare the differences between LLCs and sole proprietorships. There are more differences between these business structures than similarities. Rather than just listing bullet points, we’ll take a closer look at various categories you should evaluate. This will make it much easier for you to decide which one is right for your business.

Liability Protection

As the name implies, an LLC limits the liability of owners. LLC owners won’t be held personally liable for business debts or liabilities. If your company goes bankrupt, creditors can’t go after your personal assets (only business assets), and they are also protected in the event of a lawsuit against your company.

Since sole proprietorships are not separate entities, the owners are personally liable for any debt or legal action against the business. You could even be held responsible for any liabilities caused by an employee.

Management Structure

One or more people can own an LLC. These are known as either single-member LLCs or multi-member LLCs. In most cases, the owners will also manage the company (member-managed LLCs). However, managers can be appointed to handle the day-to-day operations (manager-managed LLCs).

The management structure of an LLC will be described in an official operating agreement, which is a legal document created during the formation process.

Sole proprietorships are simpler. The owner is the boss and in charge of everything. Sole proprietors don’t have to deal with any partners, managers, or other members.

Business Funds and Personal Funds

LLCs must have separate bank accounts for business activity and personal use. This includes separate credit cards, debit cards, checking accounts, and savings accounts. Mixing personal and business finances can result in serious penalties.

Sole proprietors do not have to maintain separate accounts for business and personal use. In the eyes of the law, sole proprietors and their businesses are one and the same. With that said, most accountants frown upon this practice and recommend using a separate account for your business. In the event of an IRS audit, this separation will make your life significantly easier. While this isn’t a fact per se, it’s assumed by many that auditors are more likely to scrutinize your records if you mix personal and business finances.

Business Name Registration

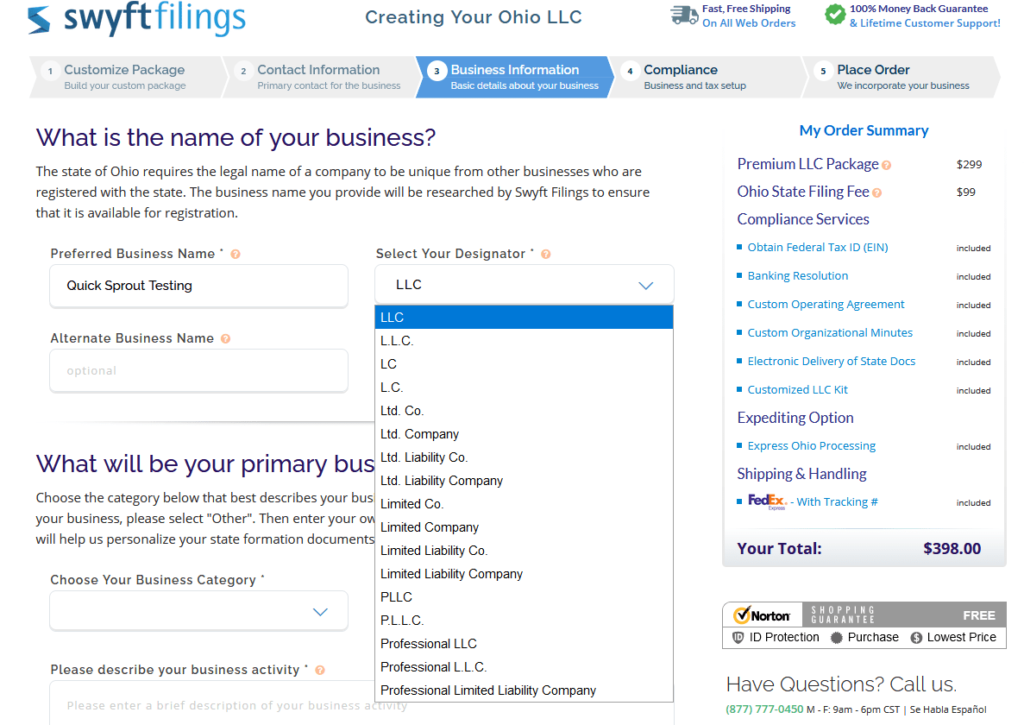

Depending on the state, the acronym “LLC” or other variations must be included in your business’s official name. Other examples include L.L.C., Limited Liability Co., Ltd Liability Co., and more. These are known as “entity designators.”

You’ll be asked to select an entity designator when you’re registering a company name. Here’s what this looks like if you’re going through that process on Swyft Filings:

Sole proprietors are not subject to these name requirements. By default, the name of a sole proprietorship will be the business owner’s actual name. However, they have the option to register a DBA (doing business as) name in their state.

LLCs can register a DBA as well.

Tax Implications

By default, LLCs are subject to pass-through taxation. The owner of an LLC has the tax liability “passed through” to their personal tax return. In short, earnings are only taxed once. However, LLCs can choose to be taxed in many different ways. This flexibility gives them the option to be taxed as a corporation, partnership, or sole proprietorship.

Similar to an LLC, sole proprietors will also benefit from pass-through taxation. Business income will be reported on the sole proprietor’s personal tax returns. Sole proprietorships are only required to pay taxes on profits (as opposed to the full income of the business). As a sole proprietor, you won’t have the option to be taxed as a corporation or partnership.

Startup Process

The requirements to register an LLC will vary slightly from state to state. But generally speaking, you’re required to file articles of organization and pay a filing fee. LLCs are required to maintain a registered agent and file annual reports with the state.

It can take weeks to form an LLC. Most people hire a lawyer or use an online business formation service to handle the paperwork and filing on their behalf.

There is no formal process required to form a sole proprietorship. However, depending on your business, you might be required to obtain a license or permit (rules vary by state). Make sure to check your state’s individual requirements, typically listed on your state government’s website.

Funding

Many businesses require capital to get up and running. Most lenders won’t approve loans for business applications if you don’t have a separate business checking account. So, LLCs might have more access to certain types of loans. However, it can be challenging to obtain a startup loan if your company has no credit. Sole proprietors with good credit could take out a personal loan or line of credit.

LLCs have an easier time taking on investors. In contrast, most investors won’t invest in a single person unless a separate legal entity is formed.

LLC Pros and Cons

Now that we’ve had a chance to compare the similarities and differences between LLCs and sole proprietorships, it’s time to take a closer look at the pros and cons of each.

LLC Advantages:

- Liability protection against business debt, lawsuits, and personal assets

- Higher level of credibility

- Flexible tax options

- Easier for multiple members and investors

- Flexible management structures

- Easier access to loans, financing, leases, and more

- Easier to hire employees

- Ability to register a business in another state

LLC Drawbacks:

- State filing requirements

- Annual fees

- Higher startup costs

- Tax returns can be more complicated

- Higher administrative costs (registered agents, accountants)

Sole Proprietorship Pros and Cons

Sole proprietorships have their fair share of perks. But do those pros outweigh the cons? Let’s take a closer look:

Sole Proprietorship Advantages:

- Easy to start

- No formal registration requirements with the state

- Owner has complete control of the business

- No directors, members, or complicated management structures

- Owner gets all business profits

- Inexpensive to form

- Business is not taxed separately from the owner

Sole Proprietorship Drawbacks:

- No liability protection

- Limited financing options

- No taxation flexibility

- Difficult to hire employees

- Owner is responsible for company losses

- Business licenses and permits are still required (depending on state and industry)

LLC vs. Sole Proprietorship: Which is Right For Your Business?

With all of this in mind, it begs the final verdict—which one is better, an LLC or a sole proprietorship?

That question can only be answered on a case-by-case basis. As previously mentioned, sole proprietorships are the most common business structure in the United States. That’s because they are easy and inexpensive to start. However, sole proprietors don’t have any liability protection. Since the business is not viewed as a separate entity, your personal assets are not safe from lawsuits or business debt.

LLCs require more work to start and are also subject to costs that don’t apply to sole proprietorships.

However, many business owners feel that the benefits of an LLC outweigh the cons. Personal liability protection is the number one advantage of starting an LLC. You can also leverage flexible tax options, different management structures, and more.

If your business has any risk for debts or lawsuits, you’ll want to protect yourself with an LLC. But if you’re running a low-risk company like a small personal blog, you can probably get away with staying a sole proprietor.

Always consult with an accountant and an attorney before determining the best business structure for your unique situation.

But this guide should be used as a reference to help keep you informed and steer you in the right direction.

from Quick Sprout https://ift.tt/2RFYJTC

via IFTTT