Disclosure: This content is reader-supported, which means if you click on some of our links that we may earn a commission.

Unless you’re independently wealthy, most small business owners need a loan at one point or another. From paying for startup costs to expansion projects, equipment, or unexpected incidents, quick access to funding will make it easier for your company to grow.

Whether you’re launching a brand new venture or own an established business, there are so many different small business lending options out there to consider.

Which small business loan is best for you? This guide contains everything you need to know on the subject.

The Top 6 Options For Small Business Loans

How to Choose the Best Small Business Loans For You

Small business loans come in all different shapes and sizes. So as you’re evaluating different options, there are specific considerations that must be examined. I’ll explain each one in greater detail below.

Lender

When most people think about getting a loan, they automatically assume that a bank is their only option. But in addition to small local banks and national bank chains, there are lots of other lenders that can provide your small business with capital.

You can explore credit unions, crowdfunding sites, P2P lenders, loan marketplaces, nonprofit lenders, and even alternative lending solutions.

The qualification requirements and loan terms will vary from lender to lender.

Loan Type

Most lenders offer multiple types of loans for small business owners. Some common small business loan types include SBA loans, lines of credit, installment loans, short term loans, equipment loans, commercial real estate loans, and merchant cash advances.

In some cases, you’ll need to provide the lender with more information about what you’ll be doing with the funds. For example, an equipment loan couldn’t be used to purchase inventory, and a commercial real estate loan couldn’t be used to buy a new vehicle.

Lines of credit are great options to have since they can be used for lots of different purposes. We’ll talk more about these different loan types in greater detail shortly.

Capital Required

The loan amount you’re seeking also needs to be taken into consideration. There’s a big difference between $5,000, $50,000, and $5 million.

Certain lenders are better for microloans and small amounts, while others are known for lending large sums of cash.

Take a look at the minimum and maximum amounts available before you apply for a loan. Generally speaking, you shouldn’t apply for more than you need (unless it’s a line of credit). Otherwise, you’ll have higher interest payments.

Minimum Qualifications

In most cases, you won’t qualify for every type of loan. So pay close attention to these terms before you apply, or you’ll just be wasting your time (and potentially hurt your credit).

Some lenders will only loan money to companies that have been in business for a certain number of years. There are also some cash flow requirements, annual revenue requirements, and business owner credit score requirements for certain loans.

Loan Terms

The loan terms are crucial when you’re evaluating different options. How soon will you need to pay the money back? What interest rates will you be paying?

Make sure you look beyond the dollar amount and take a deeper look at the terms.

Businesses with bad credit won’t have access to the lowest interest rates and loan terms. So you’ll definitely want to shop around until you’re comfortable with the options presented to you.

The Different Types of Small Business Loans

There are tons of different small business loans out there. But I want to quickly highlight the most popular options to give you a better understanding of how they work.

SBA Loan

SBA loans are backed by the Small Business Administration. This federal agency helps businesses gain access to better funding resources.

These loan amounts typically range from $50,000 to $5 million with terms from 10-25 years.

SBA loans usually have great rates (since the SBA reduces the lender’s risk), but they can be tough to qualify for. The process to apply and get approved for an SBA loan can be slow.

Business Line of Credit

Lines of credit are great for those of you who need flexibility. Instead of receiving a lump sum of cash, you can borrow up to your credit amount as needed.

Business lines of credit can range anywhere from $1,000 up to $500,000.

It’s usually easy to qualify for a line of credit if you’ve been in business for more than a year and have $50,000+ in annual revenue. Interest rates vary based on the lender, your credit score, and other qualification terms. But you’ll only pay interest on the amount you borrow on the revolving line.

Term Loan

Term loans are funded quickly. In some instances, you can receive cash within 24 hours of getting approved. It’s common for term loans to be used for working capital, equipment, operations, and more.

Some of these loans are short term and must be paid back as early as 12-24 weeks. Others have repayment terms in the 1-5 year range.

Term loans typically have fixed interest rates or flat fees, so your payments won’t increase throughout the lifetime of the loan.

Merchant Cash Advance

With a merchant cash advance program, small businesses can borrow against future earrings to secure capital. These loans are repaid with a daily percentage of your credit card sales, as previously agreed upon with the lender.

Most merchant cash advances can be used for a wide range of needs. Similar to a term loan, you can usually get access to funds quickly as well.

It’s easy to get approved for a merchant cash advance, but the interest rates are usually high.

Equipment Financing

The name is pretty self-explanatory here—the money from equipment financing must be used to purchase equipment. But it’s worth noting that the term “equipment” is pretty broad.

In addition to things like conveyor belts, forklifts, and machinery, other types of equipment like accounting software, or payment processing systems would also fall into this category.

Equipment financing is usually secured by the equipment you’re purchasing. If you fail to repay the loan, the lender can seize the equipment.

Business Credit Card

Credit cards and loans are obviously not the same. But a business credit card can potentially be a great option to finance certain purchases.

Some cards offer businesses introductory promotions like 0% APR financing within the first year of opening an account. So you can potentially buy something at 0% interest by putting it on your new credit card (assuming it’s less than your credit amount). But beyond the introductory offer, credit cards will have significantly higher interest rates than other types of loans.

You can read my reviews of the best business credit cards here.

Secured Loans

A secured loan requires some type of collateral in order for you to qualify. This is common for high-risk businesses. If the business defaults on the loan, the lender will seize the collateral.

Since secured loans don’t pose as much of a risk to lenders, the interest rates are usually low.

Unsecured Loans

An unsecured loan is the exact opposite of a secured loan. Businesses can borrow money without having to put up any collateral.

In order to qualify for an unsecured loan, your business usually needs to have a long track record of profitability and success without any liens or outstanding debts. If the lender thinks you’re a high risk to default on the loan, they might require you to secure the loan with collateral.

Crowdfunding Loans and P2P Loans

These types of loans are sourced from a pool of investors. You can get these loans from crowdfunding websites with small amounts collected from the general public or get them from alternative lending platforms where individuals offer P2P loans as a source of income.

If you can’t qualify for a traditional loan, you might consider a crowdfunding or P2P borrowing option.

#1 – Fundbox Review — Best For Short-Term Loans

Fundbox is used by 100,000+ businesses across a wide range of industries.

Technically, they offer business lines of credit. But the repayment period on the amount you borrow gets paid back over a 12 or 24-week plan, which falls into the short-term loan category.

Using Fundbox is simple, and you’ll get fast access to cash whenever you need it. To apply, you just need to connect your bank account and accounting software, so Fundbox can view your financials.

You’ll only pay for funds that you draw from your line of credit, so you can use Fundbox multiple times for various short-term loans. There’s no penalty for early repayments.

Before you withdraw funds, Fundbox gives you a transparent calculation of the principal, interest amount, and weekly payments due. So you can plan accordingly and know exactly how much you owe each week for the duration of the loan.

Fundbox is perfect for short-term situations when you need a little extra cash. It’s commonly used for late invoices payments, unplanned expenses, and to float small businesses during periods of slow sales.

Apply online, and get a decision within minutes. Funds can be transferred to your account as soon as the next business day.

#2 – Funding Circle Review — Most Versatile Loan Options

Funding Circle is an industry leader in the small business lending category. It’s a popular choice for businesses that want fast and affordable loan options.

With a single application, Funding Circle will provide you with multiple loan types and options to choose from.

Loan types and funding solutions provided by this lender include:

- SBA loans

- Business term loans

- Merchant cash advances

- Business lines of credit

- Invoice factoring

- Working capital loans

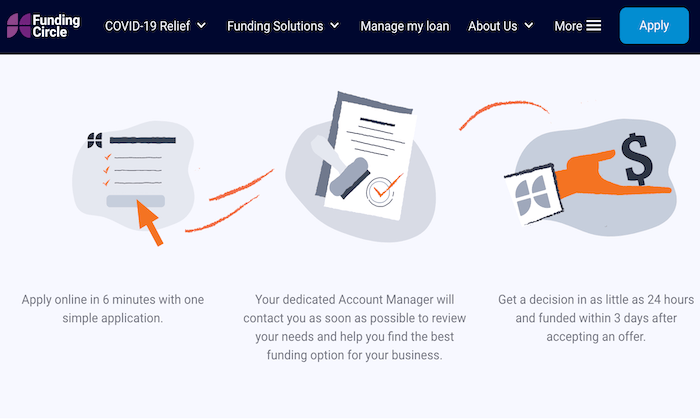

You can get a decision in less than 24 hours and gain access to funds within three days of getting approved. Funding Circle has term loans from $25,000 to $500,000 and SBA loans from $20,000 to $5 million.

I also like Funding Circle because the platform makes it easy for you to manage your loan online. Apply on their website by filling out an application—it takes just six minutes to complete.

#3 – Accion Review — Best For Startups

Accion is a nonprofit organization dedicated to helping small business owners and entrepreneurs fund their startups.

In fact, Accion is the largest nonprofit lending network in the US.

Accion offers term loans of up to $250,000 at an affordable rate. You can apply online or over the phone to get a tailored solution that fits your unique needs.

Here are some of the business types that Accion commonly lends money to:

- Women owned businesses

- Minority owned businesses

- Food and beverage businesses

- Small businesses

- Startups

- Veteran owned businesses

- Business owners with disabilities

- Green businesses

Accion also has a wide range of small business resources available to help you achieve success in your industry. With 25+ years of experience in the small business lending space, I strongly recommend Accion to startups and other businesses in the categories listed above.

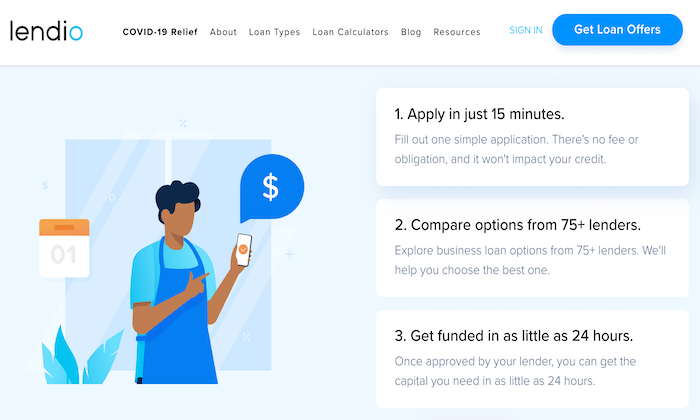

#4 – Lendio Review — Best Small Business Loan Marketplace

Lendio isn’t a small business lender. But it’s one of the most popular online marketplaces for business loans.

If you want to compare loan options from 75+ lenders with a single platform, look no further than Lendio.

This marketplace has facilitated $10+ billion in funding to 216,000+ small businesses. There is a wide range of loan types available through Lendio’s network of lenders, including:

- Startup loans

- Term loans

- Commercial mortgages

- Short term loans

- SBA loans

- Merchant cash advances

- Business lines of credit

- Business credit cards

- Equipment financing

- Accounts receivable financing

- Business acquisition loans

I also like Lendio because they provide additional resources for small business owners, like financing calculators and bookkeeping guidance.

Just fill out some quick information about your business online to get loan offers from lenders in the Lendio network.

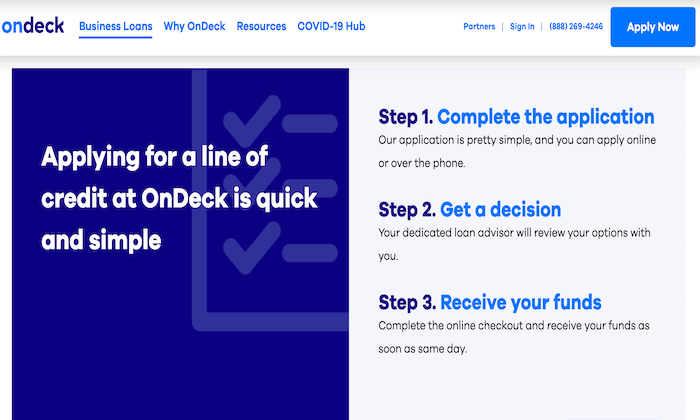

#5 – OnDeck Review — The Best For Revolving Credit

OnDeck has delivered $13+ billion to businesses across the globe. They offer term loans of up to $250,000 and business lines of credit up to $100,000.

I like OnDeck because it’s so simple. After you complete an application online or over the phone, a dedicated loan advisor will go over your options with you. OnDeck offers funding as early as the same business day.

Your line of credit from OnDeck is a great option for working capital. Only withdraw what you need, when you need it, and just pay interest for the amount borrowed.

Repay your line of credit over a 12-month term agreement with automatic weekly payments and no prepayment penalties.

To qualify, you must be in business for at least a year with a minimum personal FICO score of 600 and an annual revenue of $100,000+.

OnDeck periodically reviews your credit profile. So you can automatically qualify for higher credit line limits without having to apply for an increase. You’ll also benefit from a consolidated weekly payment on all withdrawals, so you won’t have to worry about making multiple payments.

#6 – Kiva Review — Best 0% Interest Small Business Loans

If you need a microloan and you’re not in a rush to get it, Kiva will let you borrow up to $15,000 at 0% interest—no strings attached.

As a global nonprofit, Kiva has helped 2.5+ million entrepreneurs raise $1+ billion.

The only downside of Kiva is that it takes quite a bit of time to actually get the loan. So it’s not ideal for businesses that need cash fast.

First, you need to fill out an online application that can take up to 30 minutes to complete. Then you need to prove your creditworthiness by convincing your friends and family to loan you money, which is about a 15-day process. Finally, you can go public on Kiva and make your loan visible to 1.6+ million lenders across the world (an additional 30 days).

On the positive side, you’ll have up to 36 months to repay your loan at 0% interest. It’s tough to beat that deal.

But if you’re looking for large sums of cash as fast as possible, this won’t be the best choice for your business.

Summary

If your small business needs money, there are lots of different small business loan options for you to consider.

Which one is the best?

The answer depends on a wide range of factors, like the amount you need, the loan type, lender, and more. Regardless of your situation, you can find the best loan options for your business based on my recommendations in this guide.

The post Best Small Business Loans appeared first on Neil Patel.

from Blog – Neil Patel https://ift.tt/2S4bpjI

via IFTTT